If you felt like this past month was about a decade long…

Don’t worry -you’re not the only one!

If March is anything to go by it’s going to be a very long year – so I’m going to recommend here that we all take some time to do something ultra- productive for our business.

Right now, we’re in uncharted waters. If you run a business, some of us are excited about the opportunities that will come from this crisis – and some are stuck in fear.

None of us know what’s going on, or how bad things are going to get…and a lot of us don’t really know what to do.

What’s happening out there is beyond our control… and a lot of us are scared about what this virus means for our business

Me?

On the one hand, the pain, loss and fear that I’m hearing, watching and reading about every day all over the world breaks my heart.

But on the other hand I’m excited about the opportunities that are out there waiting to be grabbed.

And I hope you are too. Because you should be.

People have needs – even in times like these.

Nobody knows when we’ll get back to normality, but we need to remember:

For centuries people have paid for things. To entertain us. To help us. To give us pleasure.

People need things, and there’s a lot of people out there who aren’t feeling the pinch right now…and can pay for stuff.

I’m a big one for controlling the controllables and not losing sleep about the other stuff you can’t change.

So if you’re a business owner feeling some pain right now, you’re no good to yourself and to your business if you can’t double down on the things that you can control.

Because doing this is step #1 to getting your business primed for life on the other side.

There’s going to be a bounce back. We don’t know when but…it’s inevitable. Normality will return.

So what can you control right now? (aside from minimising expenses, prioritising revenue generating activities – and looking after your family and your community)

I say, start thinking ‘big picture’ and set yourself up for the future by ‘de-risking’ your business.

…So what’s ‘de-risking’…and why?

Well the thing is…right now is a perfect time for many of us to take a step back and look at what our business really means to us.

For me?

I see my business as an asset that I want to make as valuable as it can possibly be.

My first business…I started in ‘07 on a shoestring with no support and no experience – and ten years later sold it for more than a million bucks.

But it was only in those last 3 years that the penny dropped and I realised that every move I made needed to be geared towards adding value to my business – building an asset (and I’m not just talking about revenue here…revenue is just one piece of the puzzle). I could have achieved so much more if that penny had dropped earlier…

So what about you?

What if you decide you want to sell your business one day/ Maybe in a couple of years…or 3…or 5?

Or…what if you decide that attracting an investor to fuel growth is the fastest way to achieve your goals?

Or…what if someone comes to you with a merger opportunity.

Or…what if you just want to play a bigger game – and work with bigger distributors of your product (who need reassurance that you have the pillars in place to deliver at scale)

If so, you should be doing everything you can to increase the value of your business (and ‘de-risking’ your business is the way to start adding that value).

So here are 7 things you can get onto right now to start boosting the value of your business – even if it’s currently getting hammered by this damn virus.

#1 Does your business have major dependencies?

Is there an unhealthy dependency on you – the owner? Do you have most of the business operating systems in your head? Do you run all team training sessions? Are you delivering the service or the majority of the service? Do you manage all the relationships?

If there is no owner…is there still a business?

If you, as the owner are the business then it doesn’t have a lot of value to others. A business that’s heavily dependent on the owner invariably raises the question from interested parties: If the owner is this business, then what exactly am I buying?

Is there a dependency on a particular one, or few clients?

If 70% of your business comes from one customer then…it’s unlikely anybody is going to invest in that business.

If this is you then…it needs to be a priority to start opening up new sales channels, new revenue streams, new markets and new types of customers.

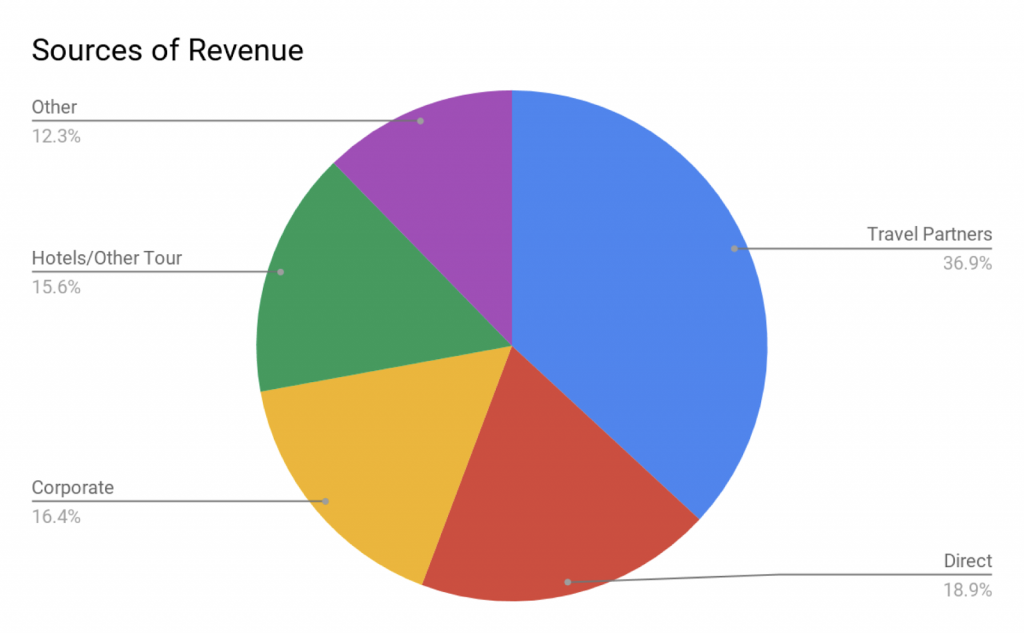

Your aim is a beautiful ‘revenue’ pie chart with a number of healthy looking pieces of pie and to move away from having an overreliance on one customer or one type of customer.

Here’s what mine looked like when I sold MPT in 2017:

Similarly, does your business have one or two major suppliers or sources of bookings, reservations or sales?

If your inbound tourists are all from China…or if you’re a corporate travel agent with a global contract with, say Price Waterhouse Cooper, or Amazon which accounts for 80% of your resources and revenue… then priority number one for you is diversification out of major client dependencies.

#2 Are your key suppliers, staff and customers all locked away with some form of an agreement?

If you haven’t got these things then I would recommend that all of your key staff need:

- A high level Position Description that both you and they have agreed to and signed off on.

- A formal, signed ‘letter of offer’ that details: remuneration, performance standard, policies & procedures and other important terms and conditions

- An incentive scheme – ideally with both company-wide and role specific objectives with a bonus payable at year’s end, structured in a way that makes it more difficult to leave.

Next, your key suppliers need to have their product or service details, inclusions and important terms, plus an agreed date of future review – all in writing.

Finally, your key customers. How can you get your most important customers to commit to you? Well…do they have an annual event that you could sponsor? Can you propose an incentive arrangement, based on a financial target, or bookings volume target (eg bookings or revenue over and above an agreed amount will trigger an ‘X’% commission payment). Can you encourage a key customer to start a ‘Preferred Supplier Program’ where – in return for their commitment to you (and the marketing and promotion of your product and service), you will provide an additional level of commission.

Get creative in ways to tie your customers to you – and this might mean tailoring an idea to each customer.

#3 Make sure your books are clean, well organised and uncomplicated.

The key when you’re looking to increase the value of your business, or to source capital, or to attract investor interest is for your financials to be as easy to understand as possible.

They’ve gotta make sense. If your books are complicated, difficult to follow, or irregular – then an interested party will likely walk away (even though the business may be in great shape and there may be no skeletons in the closet)

It’s hard to get investors interested in a business with confusing books so…keep ’em simple

#4 Do you have three consistent years of financials?

Obviously, a business with value is a business that’s profitable. But an interested party is going to look deeper than current performance and profitability. They want to see that the trend in your business is positive, not erratic…and definitely not negative.

Ideally your business is going to have a smooth upwards trend over the past 3 years, both in revenue AND in profitability.

Let’s say we’re looking at the financials of a business over 3 years – 2017, 2018 and 2019.

And let’s say 2017 was a big year, but then revenue dropped away in 2018, 2019.

The question will invariably be…so what happened in 2017? Why haven’t you been able to repeat that in 2018 and 2019? And most importantly, what’s going to happen in 2019? Is the business going to fall away further?

It’s super important for an interested party to see a nice upward trend over a minimum 3 years.

This applies also if you’re planning to sell your business on the back of one ‘break out’ year.

A potential buyer or investor generally isn’t going to be convinced to take a risk based on the pretty 12 month picture you’ve pulled together of inflated revenue and reduced costs.

A buyer will want you to demonstrate how your business has evolved, improved, become more profitable, generated more revenue over a minimum 3 years. A dramatic 1 year spike probably won’t instill enough confidence and will leave doubts (and more questions than answers). Invariably, an investor, financial institution or a buyer with doubt walks away.

When preparing your financials, you should always strip out your personal expenses first and prepare a set of normalised numbers. This means stripping out not only any personal expenses that you run through the business (travel, stationary, etc etc) but also removing any expenses that – in theory – a new owner wouldn’t inherit. You always want to be ready and prepared to present your business in the best possible light with a set of ‘normalised’ numbers.

#5 Make sure systems and processes are documented right across your business.

If you haven’t already, it adds massive value to your business. As an owner, it’s unbelievably important to get everything in your head out of your head and documented.

As a minimum, you should have:

Roles and Responsibilities and an Organisational Chart. Everyone in your business needs to be 100% clear on exactly what their role is, what they and everybody else in the business are responsible for so there is no role confusion – even if there are only two of you right now.

Sales and Marketing Process. This entire process needs to be documented from end to end: from the receipt of and responding to an enquiry, follow up of enquiries, delivery of a booking confirmation document, receipt of payment, handover to operations, feedback and review request, plus internal feedback.

Operations Processes. I was HUGE on documenting our operational processes when I was running my travel business. Our end goal was for nobody to have to ask the same question twice. If myself or my Operations Manager fielded the same question more than once, then that was our cue to document a process, so that if we ever got the same question again…the answer was simply “go and read the manual”..

#6 Develop a blueprint for taking the business to the next level. An interested party wants to know: What would you do if you had the resources at hand and the interest in staying to take this business to the next level? You want to get people excited about the potential in this business that just needs unlocking. People want to know how this business can be taken to the next level – and to the level above that. So best you start putting some thought into this now.

#7 Negotiate a long lease now – if the location from which you operate is important to the business. Now is the time to have that chat with the landlord and extend your lease for as long as is possible. It can create a massive stumbling block if you don’t get onto this until the time that everything’s riding on it – and it will be a big tick from an interested party.

From experience, it’s the little things like a simple lease extension – when you’re relying on something seemingly straightforward, but beyond your control – that can threaten to derail a deal.

So hopefully I’ve given you some inspiration and a ‘road map’ for you to start increasing the value of what could become the biggest asset you’ll ever own.